DEFINITION:

The Performance Score is a comprehensive metric (0-100) that combines multiple risk-adjusted metrics into a single number. Learn how it's calculated and how to interpret it.

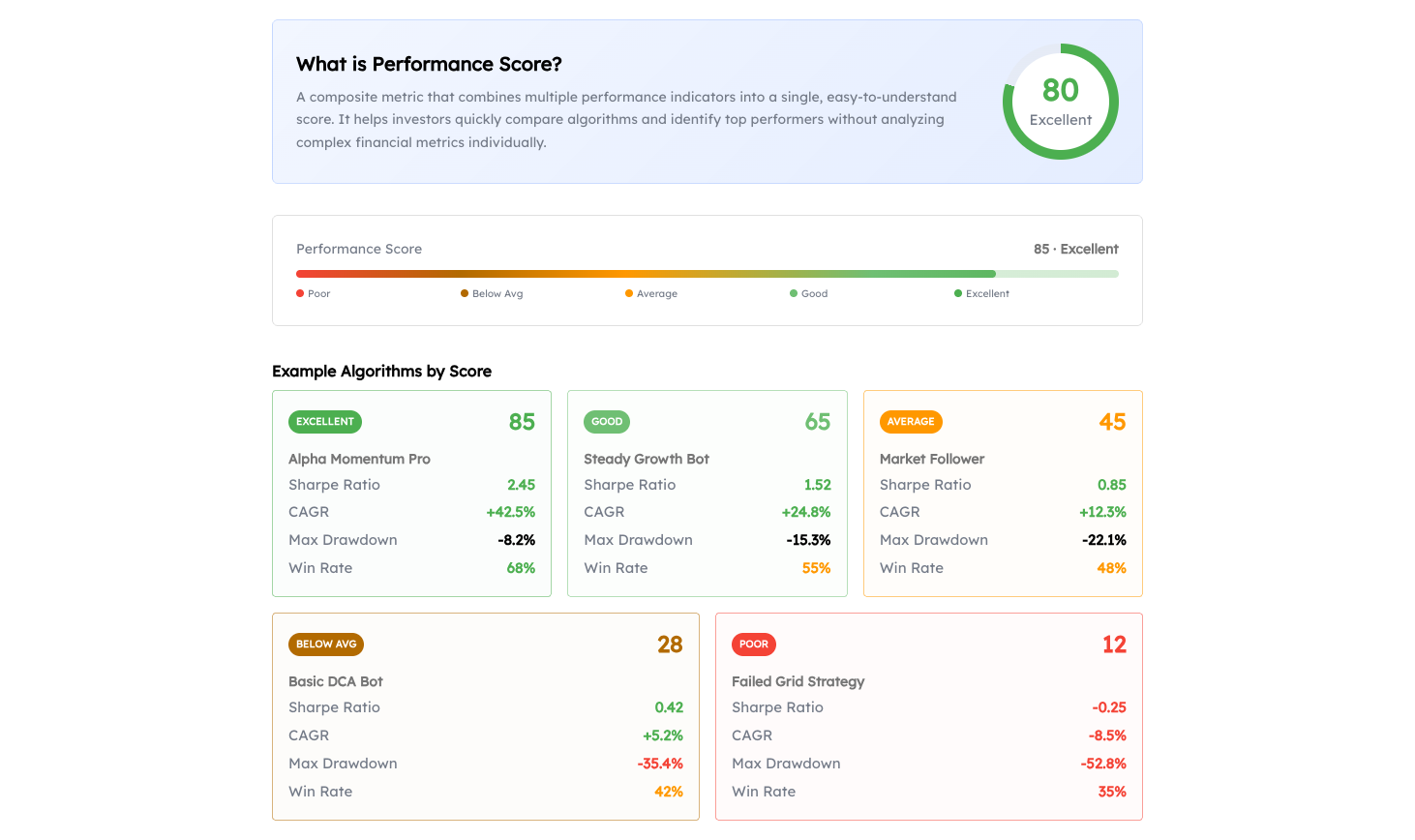

Performance Score

The Performance Score is a comprehensive metric that provides a single number (0-100) representing the overall quality of a trading bot's performance. It combines multiple risk-adjusted metrics into one easy-to-understand score, making it simple to compare different trading strategies at a glance.

Why Use a Performance Score?

Evaluating a trading bot requires analyzing many different metrics—returns, risk, consistency, and resilience. Each metric tells only part of the story:

- High returns might come with excessive risk

- Low drawdowns might mean overly conservative strategies

- High win rates don't guarantee profitability

The Performance Score solves this by combining the most important metrics into a single, balanced score that considers all aspects of performance.

How Is the Performance Score Calculated?

The Performance Score is a weighted average of six normalized metrics:

| Metric | Weight | What It Measures |

|---|---|---|

| Sharpe Ratio | 25% | Risk-adjusted return (most widely used) |

| Sortino Ratio | 20% | Downside risk-adjusted return |

| Calmar Ratio | 15% | Return relative to maximum drawdown |

| CAGR | 15% | Compound annual growth rate |

| Win Rate | 15% | Percentage of profitable trades |

| Recovery Factor | 10% | Ability to recover from losses |

Normalization Process

Each metric is normalized to a 0-100 scale before applying weights:

- Sharpe Ratio: -2 to 4 → 0 to 100

- Sortino Ratio: -2 to 4 → 0 to 100

- Calmar Ratio: 0 to 5 → 0 to 100

- CAGR: -50% to 100% → 0 to 100

- Win Rate: Already 0-100%

- Recovery Factor: 0 to 5 → 0 to 100

The Formula

Performance Score = (Sharpe × 0.25) + (Sortino × 0.20) + (Calmar × 0.15)

+ (CAGR × 0.15) + (WinRate × 0.15) + (Recovery × 0.10)

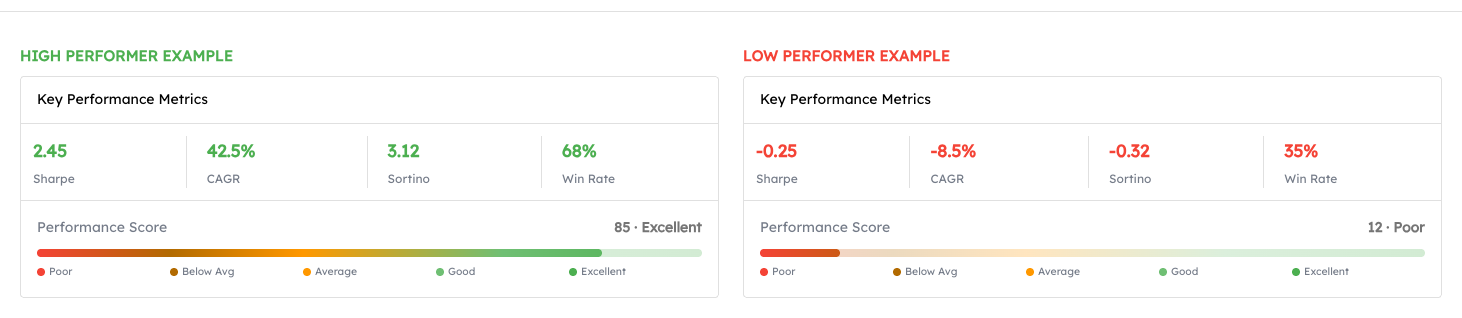

Interpreting the Performance Score

| Score Range | Rating | Interpretation |

|---|---|---|

| 80-100 | Excellent | Outstanding performance across all metrics |

| 60-79 | Good | Strong performance with minor weaknesses |

| 40-59 | Average | Moderate performance, room for improvement |

| 20-39 | Below Average | Significant concerns in multiple areas |

| 0-19 | Poor | Major issues requiring attention |

Component Metrics Explained

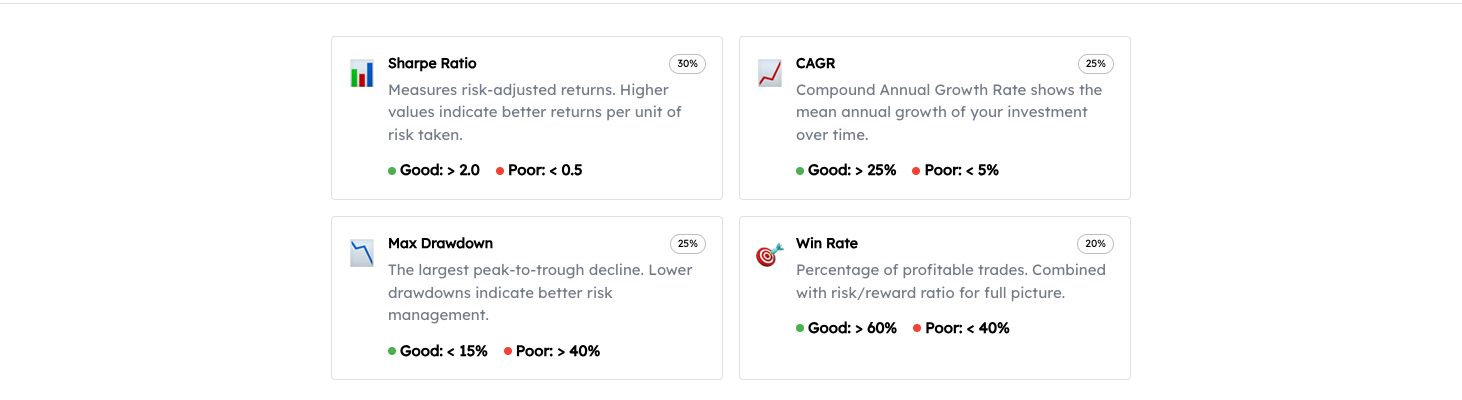

Sharpe Ratio (25% Weight)

The Sharpe Ratio measures risk-adjusted returns by comparing excess returns to volatility. A higher Sharpe ratio indicates better returns per unit of risk.

- Above 2.0: Excellent

- 1.0 to 2.0: Good

- 0.5 to 1.0: Average

- Below 0.5: Poor

Sortino Ratio (20% Weight)

The Sortino Ratio is similar to Sharpe but only considers downside volatility. This makes it particularly useful for strategies that have asymmetric return distributions.

Calmar Ratio (15% Weight)

The Calmar Ratio divides the CAGR by the maximum drawdown. It measures how well the strategy performs relative to its worst-case scenario.

CAGR (15% Weight)

The Compound Annual Growth Rate represents the average annual return if profits were reinvested. It provides a standardized way to compare returns across different time periods.

Win Rate (15% Weight)

The Win Rate measures the percentage of profitable trades. While high win rates don't guarantee profitability, they indicate trading consistency.

Recovery Factor (10% Weight)

The Recovery Factor measures how quickly a strategy recovers from drawdowns. A higher recovery factor indicates greater resilience and the ability to bounce back from losses.

Why These Weights?

The weighting system prioritizes risk-adjusted metrics:

-

Sharpe Ratio (25%) gets the highest weight because it's the most comprehensive single measure of risk-adjusted performance and is universally used in the investment industry.

-

Sortino Ratio (20%) receives significant weight because it specifically penalizes downside risk, which matters most to investors.

-

Calmar Ratio (15%) ensures strategies with large drawdowns are appropriately penalized.

-

CAGR (15%) represents raw returns—ultimately what investors seek.

-

Win Rate (15%) indicates trading consistency and psychological comfort.

-

Recovery Factor (10%) measures resilience but receives lower weight since it's partially captured by other metrics.

Limitations

While the Performance Score is a powerful tool, keep these limitations in mind:

- Historical basis: The score is based on past performance, which doesn't guarantee future results

- Time sensitivity: Recent performance may differ from the overall score

- Market conditions: A strategy might score well in certain market conditions but poorly in others

- Strategy type: Different strategy types (trend-following vs. mean-reversion) may have different typical scores

Best Practices

-

Compare similar strategies: Use the score to compare strategies with similar investment horizons and risk profiles

-

Look at the components: A high overall score with one weak component might indicate a specific risk

-

Consider market conditions: Evaluate how the score changes across different market regimes

-

Monitor over time: Track how the score evolves as the strategy continues trading

-

Combine with qualitative analysis: The score should complement, not replace, understanding the strategy's logic

Conclusion

The Performance Score provides a quick, comprehensive way to evaluate trading bot performance. By combining multiple metrics with appropriate weights, it offers a balanced view of returns, risk, consistency, and resilience. Use it as a starting point for comparison, then dive deeper into individual metrics for strategies that interest you.

Table of Contents

Performance Score

Why Use a Performance Score?

How Is the Performance Score Calculated?

Interpreting the Performance Score

Component Metrics Explained

Why These Weights?

Limitations

Best Practices

Conclusion

About the Author

Marc van Duyn

Founder & CEOMarc is the Founder and CEO of Finterion. He is passionate about making algorithmic trading accessible to everyone.